FICO Credit Score Back Up to 760: Big Yawn...

Some good news and some bad news this month. First, the bad news.

The mother of my child moved out into her own condo, so, even though I am enjoying the extra space, stress relief and the freedom, I have agreed to pay $300 per month in child support.

$300 per month is too high, in my opinion, considering the circumstances. First of all, the mother of my child has a full time job with excellent benefits. She doesn't have to make car payments on her car (as I do), because she owns it, thanks to me. When her car broke down a couple of years ago, I gave her my very reliable and well-maintained car, and I bought another used car for me. Her insurance payments are very cheap as well -- less than $500 per year.

Now, don't get me wrong: I'm not trying to make a big deal out of my car donation, because it's really not that big a deal to me. I'm just laying down the facts here, and I think it's important to note the source of her assets.

Another reason why I feel that $300 per month is too much: our child -- I'll refer to her as TK from now on -- is in preschool, and I am paying for her tuition, which is $135 per week, or $540 per month.

Furthermore, it's not like TK is with her mother all the time. I pick up TK from school, and she spends all day with me every Friday (her preschool is 4 days per week), and she stays with me every other weekend.

Now, considering all these factors, I thought that $200 per month plus TK's tuition payments was fair. We debated the issue for about half an hour -- without any shouting, which was a welcome surprise -- and, in the end, I acquiesced and agreed to $300 per month. The way I see it, the bottom line is that we are in a critical transition period right now, and I really don't want to do anything to exacerbate the tensions that inevitably manifest themselves when a home is newly broken; my daughter can be surprisingly mature at times, but she's also very sensitive. My baby girl means a lot to me, so as long the money I'm providing is being used for food, clothes, weekend outings and trips to the hairdresser, I'm OK with it (I don't think I'm being a miser, but if you think I'm just being a cheap bastid', then feel free to post your comments below. I'm open to all rational arguments!)

So I'll be paying TK's mother by check tomorrow, and from February on I'll be making payments via a prepaid debit card, so that I can track all spending online. I'm not just being paranoid. When TK's mom was living with me, she would order stuff from QVC and the Home Shopping Network sometimes. Did I have problem with the spending? No, not at all. What did bother me, however, was the way she would spend money on items, then totally trash them or even throw them away a few weeks later. That kind of nonsense just boils my blood. That kind of spending is, in my opinion, a sign of a serious psychological problem -- possibly depression -- but that's a subject for a another blog.

I was hoping to fatten my savings account this year, as I'm getting too old to have such a puny balance in my savings account. But I guess I'll just have to work harder, and chase the dollar with even more zeal in order to maintain myself and my obligations.

One way I'm saving money is by using space heaters instead of the electric heating system that's installed in my place. My apartment's built-in heating system is a real hog at 8 kilowatts. When I got my first electric bill back a few years ago, it was a staggering $600 (December used to be a cold month in the Northeast U.S.) so I was highly motivated to find another heating solution (I was also motivated by my breathing problems, which are almost always exacerbated by built-in heating systems, no matter how well they are cleaned.) I turn my space heaters on when I need them, or when the nights are really cold, and this works very well for me. My heating bill now averages about $157 during the winter months, much less during the warm months, which is pretty darn good considering that I work from home (my computers actually produce enough heat to keep my home office toasty most of the time; of course, my office gets a bit too sticky during August, and I sometimes have to (grudgingly) power up my portable air conditioner.) I usually turn all my space heaters on full blast when my daughter is staying with me, as she has a habit of stripping down and running around the house with just her panties on.

I have to laugh at myself sometimes when I'm home alone. I'm so keen about saving money that my office is often the only warm room in the house during the cold months. This makes for some very eye-opening trips to the bathroom: who needs coffee when you've got freezing cold floors and toilet seats.

It's funny: when I was in high school, I never imagined that I would grow up to become the kind of person who thinks about money every day, but that's who I am now. I don't think an hour goes by without me thinking about ways that I can boost my income by another $10,000 per month, or ways that I can reduce my daily living expenses. Oh well.

OK, and now for the good news.

One of my businesses did surprisingly well during the holidays, so for February and March (it takes a while for my earnings to filter through to my bank account), I'll have some extra cash to play with.

As noted above, I don't think I'll be able to play catch-up with my savings situation, because my pending windfall has already been earmarked. I'm going to

But I am very tired of my personal credit card debt. I'm bored with it. I'm sick of it!

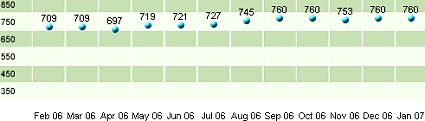

My FICO® credit score, provided by TransUnion, jumped back up from 753 to 760 last month, and it stayed at 760 this month (boring!) My credit score hasn't experienced a serious jump since September, 2006. I'm itching for the kind of fix that only a 10+ point jump to my FICO score can provide.

Yep, my credit score is good enough that I could easily qualify for yet another 12-15 month 0% balance transfer offer, which would allow me to avoid paying interest on my personal credit card debt for another year or so. But, the bottom line: transferring my debt via a 0% APR deal is just moving my debt around, and I'm tired of it. The banks and credit card companies have made some good money off my debt, but it's time to turn off the music and kick everybody out: the party is over. I now have the power to eliminate all of my personal credit card debt and some of my business credit card debt, and that's exactly what I'm going to do.

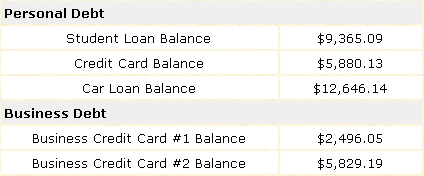

Here's what my current debt situation looks like:

Paying off my personal credit card debt should give my FICO credit score a huge boost, and should get me to my goal of an 800+ credit score sooner than I had originally planned (If bringing a personal credit card balance of $5,800 down to zero doesn't boost my FICO score above 800, then I will certainly lose faith in the system.)

At first, I was thinking of paying off my car loan. It would feel great to own my vehicle and get my title back into my fireproof safe where it belongs. It would also be great to get rid of the almost $390 per month I pay on my car loan; that's money that could ease the stress of my nascent $300-per-month child support payments. But the APR associated with my car loan is 6.25%, which is pretty good considering that the national Prime Rate is 8.25% right now. I'm paying higher than 6.25% on some of my other debts, so paying off my car loan is out, for now.

I then considered paying off my student loan debt. When I consolidated my student loan several years ago, I got an APR of 8.25%. Lots of people are consolidated at half the APR I'm paying these days, which makes me feel like I'm getting ripped off. But my student loan payments aren't stressful, and my credit card debt is more of a priority for me.

So, by March of this year, I will have completely wiped out my personal credit card debt, wiped out the debt on Business Credit Card #1, and made some major progress (i.e. cut the balance in half) with the debt on Business Credit Card #2. Business is kinda' slow right now, but if my new marketing push is successful, I plan on making some large payments toward my student loan and my car loan, so as to eliminate at least some of the interest I'll pay on those loans.

That's it for now. Remember: comments are always welcome.

Here's an updated image of my charted credit score:

The mother of my child moved out into her own condo, so, even though I am enjoying the extra space, stress relief and the freedom, I have agreed to pay $300 per month in child support.

$300 per month is too high, in my opinion, considering the circumstances. First of all, the mother of my child has a full time job with excellent benefits. She doesn't have to make car payments on her car (as I do), because she owns it, thanks to me. When her car broke down a couple of years ago, I gave her my very reliable and well-maintained car, and I bought another used car for me. Her insurance payments are very cheap as well -- less than $500 per year.

Now, don't get me wrong: I'm not trying to make a big deal out of my car donation, because it's really not that big a deal to me. I'm just laying down the facts here, and I think it's important to note the source of her assets.

Another reason why I feel that $300 per month is too much: our child -- I'll refer to her as TK from now on -- is in preschool, and I am paying for her tuition, which is $135 per week, or $540 per month.

Furthermore, it's not like TK is with her mother all the time. I pick up TK from school, and she spends all day with me every Friday (her preschool is 4 days per week), and she stays with me every other weekend.

Now, considering all these factors, I thought that $200 per month plus TK's tuition payments was fair. We debated the issue for about half an hour -- without any shouting, which was a welcome surprise -- and, in the end, I acquiesced and agreed to $300 per month. The way I see it, the bottom line is that we are in a critical transition period right now, and I really don't want to do anything to exacerbate the tensions that inevitably manifest themselves when a home is newly broken; my daughter can be surprisingly mature at times, but she's also very sensitive. My baby girl means a lot to me, so as long the money I'm providing is being used for food, clothes, weekend outings and trips to the hairdresser, I'm OK with it (I don't think I'm being a miser, but if you think I'm just being a cheap bastid', then feel free to post your comments below. I'm open to all rational arguments!)

So I'll be paying TK's mother by check tomorrow, and from February on I'll be making payments via a prepaid debit card, so that I can track all spending online. I'm not just being paranoid. When TK's mom was living with me, she would order stuff from QVC and the Home Shopping Network sometimes. Did I have problem with the spending? No, not at all. What did bother me, however, was the way she would spend money on items, then totally trash them or even throw them away a few weeks later. That kind of nonsense just boils my blood. That kind of spending is, in my opinion, a sign of a serious psychological problem -- possibly depression -- but that's a subject for a another blog.

I was hoping to fatten my savings account this year, as I'm getting too old to have such a puny balance in my savings account. But I guess I'll just have to work harder, and chase the dollar with even more zeal in order to maintain myself and my obligations.

One way I'm saving money is by using space heaters instead of the electric heating system that's installed in my place. My apartment's built-in heating system is a real hog at 8 kilowatts. When I got my first electric bill back a few years ago, it was a staggering $600 (December used to be a cold month in the Northeast U.S.) so I was highly motivated to find another heating solution (I was also motivated by my breathing problems, which are almost always exacerbated by built-in heating systems, no matter how well they are cleaned.) I turn my space heaters on when I need them, or when the nights are really cold, and this works very well for me. My heating bill now averages about $157 during the winter months, much less during the warm months, which is pretty darn good considering that I work from home (my computers actually produce enough heat to keep my home office toasty most of the time; of course, my office gets a bit too sticky during August, and I sometimes have to (grudgingly) power up my portable air conditioner.) I usually turn all my space heaters on full blast when my daughter is staying with me, as she has a habit of stripping down and running around the house with just her panties on.

I have to laugh at myself sometimes when I'm home alone. I'm so keen about saving money that my office is often the only warm room in the house during the cold months. This makes for some very eye-opening trips to the bathroom: who needs coffee when you've got freezing cold floors and toilet seats.

It's funny: when I was in high school, I never imagined that I would grow up to become the kind of person who thinks about money every day, but that's who I am now. I don't think an hour goes by without me thinking about ways that I can boost my income by another $10,000 per month, or ways that I can reduce my daily living expenses. Oh well.

OK, and now for the good news.

One of my businesses did surprisingly well during the holidays, so for February and March (it takes a while for my earnings to filter through to my bank account), I'll have some extra cash to play with.

As noted above, I don't think I'll be able to play catch-up with my savings situation, because my pending windfall has already been earmarked. I'm going to

- Maintain a decent quality of life.

- Take care of my familial responsibilities.

- Pay down my personal and business debt.

- Send my father $1,000 (he recently had surgery and needs some cash. I can empathize: I had a tonsillectomy back in April of last year.)

- Maybe, just maybe, take a small, working vacation (my last real vacation was in 1999.)

But I am very tired of my personal credit card debt. I'm bored with it. I'm sick of it!

My FICO® credit score, provided by TransUnion, jumped back up from 753 to 760 last month, and it stayed at 760 this month (boring!) My credit score hasn't experienced a serious jump since September, 2006. I'm itching for the kind of fix that only a 10+ point jump to my FICO score can provide.

Yep, my credit score is good enough that I could easily qualify for yet another 12-15 month 0% balance transfer offer, which would allow me to avoid paying interest on my personal credit card debt for another year or so. But, the bottom line: transferring my debt via a 0% APR deal is just moving my debt around, and I'm tired of it. The banks and credit card companies have made some good money off my debt, but it's time to turn off the music and kick everybody out: the party is over. I now have the power to eliminate all of my personal credit card debt and some of my business credit card debt, and that's exactly what I'm going to do.

Here's what my current debt situation looks like:

Paying off my personal credit card debt should give my FICO credit score a huge boost, and should get me to my goal of an 800+ credit score sooner than I had originally planned (If bringing a personal credit card balance of $5,800 down to zero doesn't boost my FICO score above 800, then I will certainly lose faith in the system.)

At first, I was thinking of paying off my car loan. It would feel great to own my vehicle and get my title back into my fireproof safe where it belongs. It would also be great to get rid of the almost $390 per month I pay on my car loan; that's money that could ease the stress of my nascent $300-per-month child support payments. But the APR associated with my car loan is 6.25%, which is pretty good considering that the national Prime Rate is 8.25% right now. I'm paying higher than 6.25% on some of my other debts, so paying off my car loan is out, for now.

I then considered paying off my student loan debt. When I consolidated my student loan several years ago, I got an APR of 8.25%. Lots of people are consolidated at half the APR I'm paying these days, which makes me feel like I'm getting ripped off. But my student loan payments aren't stressful, and my credit card debt is more of a priority for me.

So, by March of this year, I will have completely wiped out my personal credit card debt, wiped out the debt on Business Credit Card #1, and made some major progress (i.e. cut the balance in half) with the debt on Business Credit Card #2. Business is kinda' slow right now, but if my new marketing push is successful, I plan on making some large payments toward my student loan and my car loan, so as to eliminate at least some of the interest I'll pay on those loans.

That's it for now. Remember: comments are always welcome.

Here's an updated image of my charted credit score:

Labels: 760, child_support, credit_score, fico, separation

|

--> CLICK HERE TO VOTE IN THE DEBT POLL <--

|

posted by FedPrimeRate.com | 1/30/2007 05:46:00 PM

![]()

![]()

5 Comments:

Maybe its just me and I don't know crap but I don't think child support is about affordability. Isn't it about the child and responsibility to help care for that child?

Just a thought. I don't know anything about your circumstances and nothing about you. Delete this if it bothers you.

Take Care

Michael

> Isn't it about the child and

> responsibility to help care

> for that child?

If I could trust the mother of my child with finances then I wouldn't worry about child support. My child's mom has spending issues, and she lies whenever she isn't comfortable with the truth. In fact, just last week, I found out that she didn't have any milk in her fridge. Why? Too tired/lazy to go to the supermarket and get it.

You see, it's very hard to give someone money when you don't trust that person. Very hard. I'd rather pay her less in child support, and put the money in the bank, so that I can afford to hire a nanny sometime this year. That way my child can live with me and I won't have to worry about how she's doing.

I am a woman but sometimes I get miffed by golddiggers and then on the other hand I also get miffed by men who choose a woman for all the wrong reasons. That having been said, I think that you have solved the problem by organising a debit card, whereby you will monitor purchases. I think you are a good man but I think that you would drive me crazy too with all that frugality (is there such a word lol).

Be Blessed

> I think you are a good man

> but I think that you would

> drive me crazy too with all

> that frugality...

I'm really not that frugal. I try to be as frugal and efficient as my personality permits, but I often spend more than I should on things like my car and food (I don't eat a lot, I just like high-quality eats.)

I have friends who are so frugal you wouldn't believe it. These guys are wealthy -- no doubt --, but they are also very much alone. I think few things turn a woman off more than a super-cheap guy. Yup.

You made me laugh with your blog. its refreshingly honest and funny. keep it up. You sound like you've got your stuff together in terms of your debt

I should get some pointers from you altho im not in the states so you wouldnt even know australias laws. Well all the best with the child payments you sound like you truly love you child. cheers

Post a Comment

Links to this post:

Create a Link

<< Home