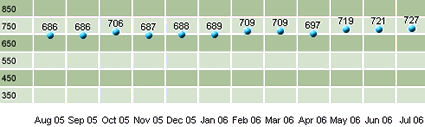

FICO Credit Score Gets A 6 Point Raise: Now @ 727

Folks, in my opinion, the system works. Pay all your bills on time, spend your money wisely, shred all documents that contain any sensitive information, and your credit score will rise. Being responsible in matters of money lets the banks know that you "get it," and they respond by offering you the best deals on loans, credit cards, etc. It's really that simple.

Just checked my FICO® credit score to find a new record high: 727. I managed to squeeze out a $700+ payment on one of my Citibank consumer credit cards earlier this month, bringing the balance on that particular card down to zero. So now I am down to one consumer card with a balance, and I plan on transferring that balance to another account in the near future, as there are still plenty of top-notch 0% balance transfer offers out there.

Instinctual Budgeting

I'm going to coin a new phrase, people, right here, right now: "Instinctual Budgeting." That's what I rely on, and it works quite well for me. Some of my friends use complex budgeting systems in order to stay on track with their finances. I respect their discipline, but it's not for me: I simply don't have the time for that. Even if I were to use a sophisticated software program that made budgeting both very easy and very efficient, it would still take up too much of my precious time!

Basically, I know exactly how much my life costs on a daily basis. Rent, phone, cable, cell, Internet, food, energy, etc. Very easy to calculate, since my bills don't vary that much. I also know how much I make on a typical day. Every month, I deposit between $1,500 and $2,000 into my savings account. If for some reason I am not able to deposit at least $1,500 in a particular month, then I cut back on the number of meals I eat outside my apartment, and make up for the lost ground by depositing more than $2,000 the following month.

That's it, really. Sometimes, when I'm at Wal-Mart picking up something I need like deodorant or plastic cups, I get the urge to do a little impulse spending, like pickup a cool gadget or an extra, high velocity fan (it's been very hot this week!) When I get the urge, a little alarm bell goes off in my head, and the urge is almost always defeated after the frugal side of my brain asks the spendthrift side, "Do you really need that item?"

Yep, it's all about sticking to what you need, and spending on what you want on rare occasions.

Here's some advice for anyone who's having trouble controlling their spending: every time you want to buy something, ask yourself if the item or service you are about to spend your hard-earned money on has real value to you. I've saved myself from countless impulse purchases by asking that question whenever I get the itch.

Of course, I'm a guy, so it's relatively easy for me to be thrifty. I shave my own head every two weeks (my hair grows fast.) I have a one pair or sandals--which I wear way too often, one pair of athletic shoes and one pair of black dress shoes. I go clothes shopping every 3-5 years, though I do pickup a new underwear, undershirts and socks every 6-9 months or so. I spend more on my baby girl than I do on myself, and that's the way it should be, IMO.

My plan is to get to a point where I can comfortably deposit between $3,500 and $5,000 into my savings account each and every month. The only obstacles preventing me from doing that right now are my credit card debts and my student loans debts. If all goes well, I should be able to deposit at least $3,500 per month by this time next year. Wish me luck!

Here's the latest screen shot image of my charted FICO credit score:

That's it for now. Hopefully my FICO score will experience another increase at the end of August. I'll share the numbers as soon as I get them. Thanks much for reading.

Just checked my FICO® credit score to find a new record high: 727. I managed to squeeze out a $700+ payment on one of my Citibank consumer credit cards earlier this month, bringing the balance on that particular card down to zero. So now I am down to one consumer card with a balance, and I plan on transferring that balance to another account in the near future, as there are still plenty of top-notch 0% balance transfer offers out there.

Instinctual Budgeting

I'm going to coin a new phrase, people, right here, right now: "Instinctual Budgeting." That's what I rely on, and it works quite well for me. Some of my friends use complex budgeting systems in order to stay on track with their finances. I respect their discipline, but it's not for me: I simply don't have the time for that. Even if I were to use a sophisticated software program that made budgeting both very easy and very efficient, it would still take up too much of my precious time!

Basically, I know exactly how much my life costs on a daily basis. Rent, phone, cable, cell, Internet, food, energy, etc. Very easy to calculate, since my bills don't vary that much. I also know how much I make on a typical day. Every month, I deposit between $1,500 and $2,000 into my savings account. If for some reason I am not able to deposit at least $1,500 in a particular month, then I cut back on the number of meals I eat outside my apartment, and make up for the lost ground by depositing more than $2,000 the following month.

That's it, really. Sometimes, when I'm at Wal-Mart picking up something I need like deodorant or plastic cups, I get the urge to do a little impulse spending, like pickup a cool gadget or an extra, high velocity fan (it's been very hot this week!) When I get the urge, a little alarm bell goes off in my head, and the urge is almost always defeated after the frugal side of my brain asks the spendthrift side, "Do you really need that item?"

Yep, it's all about sticking to what you need, and spending on what you want on rare occasions.

Here's some advice for anyone who's having trouble controlling their spending: every time you want to buy something, ask yourself if the item or service you are about to spend your hard-earned money on has real value to you. I've saved myself from countless impulse purchases by asking that question whenever I get the itch.

Of course, I'm a guy, so it's relatively easy for me to be thrifty. I shave my own head every two weeks (my hair grows fast.) I have a one pair or sandals--which I wear way too often, one pair of athletic shoes and one pair of black dress shoes. I go clothes shopping every 3-5 years, though I do pickup a new underwear, undershirts and socks every 6-9 months or so. I spend more on my baby girl than I do on myself, and that's the way it should be, IMO.

My plan is to get to a point where I can comfortably deposit between $3,500 and $5,000 into my savings account each and every month. The only obstacles preventing me from doing that right now are my credit card debts and my student loans debts. If all goes well, I should be able to deposit at least $3,500 per month by this time next year. Wish me luck!

Here's the latest screen shot image of my charted FICO credit score:

That's it for now. Hopefully my FICO score will experience another increase at the end of August. I'll share the numbers as soon as I get them. Thanks much for reading.

Labels: 727, budgeting, credit_score, fico

|

--> CLICK HERE TO VOTE IN THE DEBT POLL <--

|

posted by FedPrimeRate.com | 7/31/2006 01:35:00 AM

|

0 comments

links to this post

![]()

![]()