Fair Isaac's Revamped Credit Scoring System: FICO 08

So, I may not have to write a letter to Fair Isaac complaining about the FICO credit scoring system after all. Fair Isaac is in the process of rolling out a new version of FICO called FICO 08.

Here are two clips from a WSJ article:

Here are two clips from a WSJ article:

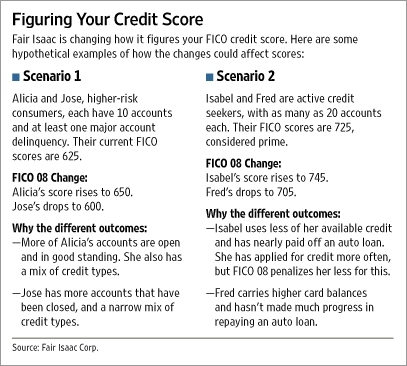

"...Higher-risk borrowers may find it tougher to get credit, while those with less-risky profiles -- though they may have gotten approved for credit accounts in the past -- will start to get better deals from lenders.

Two people with the same FICO score currently could see their scores diverge under the new system. One possible reason: FICO 08 gives more points to consumers who maintain a variety of credit types, such as credit cards, a mortgage and auto loan, because it shows they can manage payments on different kinds of loans. On the other hand, the new scoring system penalizes to a greater degree borrowers who use a high percentage of their available credit.

FICO 08 also will draw greater distinctions among different borrowers who are at least 90 days late in making a loan payment, known as a serious delinquency. Traditionally, many credit-scoring models grouped subprime consumers into one general category. But Fair Isaac says its new model will give a higher score to a borrower in arrears if they also have a number of other credit accounts in good standing. Conversely, a person's score could drop if he or she has multiple delinquent accounts.

'Overall, more consumers will see their FICO scores go up slightly than will see their scores drop,' says Tom Quinn, vice president of global scoring solutions for Fair Isaac..."

"...FICO 08 also aims to curtail the growing business of allowing people to polish their credit by "piggybacking" on someone else's good credit history. In recent years, credit-repair Web sites have sprung up that arrange for subprime consumers to boost their scores by becoming authorized users on accounts held by strangers with better credit. When scoring a consumer, FICO 08 won't take into consideration credit-card accounts for which that person is an authorized user. But the move also will hurt legitimate users: People who give a credit card to a child or a spouse as an authorized user to help boost their credit score..."

Labels: credit_score, fico

|

--> CLICK HERE TO VOTE IN THE DEBT POLL <--

|

posted by FedPrimeRate.com | 12/21/2007 02:31:00 PM

|

3 comments

links to this post

![]()

![]()

First, these machines are very handsome. They are perfectly matched in color, size and form, and they are stackable (the stackable feature is very important to me since my laundry closet is quite narrow.) The Best Buy delivery guys did a great job installing the machines; the installation was challenging due to the tight closet. When stacked, the two machines just barely fit inside my closet vertically, which was a huge relief. But the front ends of the machines extended out beyond the closet door. My solution: I just removed the closet door, which was very easy. These babies are so pretty that I probably wouldn't have closed the closet door anyway.

First, these machines are very handsome. They are perfectly matched in color, size and form, and they are stackable (the stackable feature is very important to me since my laundry closet is quite narrow.) The Best Buy delivery guys did a great job installing the machines; the installation was challenging due to the tight closet. When stacked, the two machines just barely fit inside my closet vertically, which was a huge relief. But the front ends of the machines extended out beyond the closet door. My solution: I just removed the closet door, which was very easy. These babies are so pretty that I probably wouldn't have closed the closet door anyway. These washers use very little water, which is perfect for me because the plumbing system in this place can't handle the large volume of water that most top loading washing machines use. Less water also means less energy used per load, which saves on my electric bill.

These washers use very little water, which is perfect for me because the plumbing system in this place can't handle the large volume of water that most top loading washing machines use. Less water also means less energy used per load, which saves on my electric bill. I went to take a shower this morning, and found that I had no hot water. For me, taking a cold shower is tantamount to torture, so I immediately called the management for help. The maintenance manager, Don, was at my door within 20 minutes. He checked my water heater and found it dead, which was surprising because it was less than 5 year old. There was water all over the heater and on the floor, so it was a corrosion issue. He told me that I could wait until the next day for a new heater, or he could install one right now, but I would be without water -- both hot and cold -- for about 6 hours (it takes a while to drain a water heater, and for my place you have to shut down the entire plumbing system in order to get the job done.)

I went to take a shower this morning, and found that I had no hot water. For me, taking a cold shower is tantamount to torture, so I immediately called the management for help. The maintenance manager, Don, was at my door within 20 minutes. He checked my water heater and found it dead, which was surprising because it was less than 5 year old. There was water all over the heater and on the floor, so it was a corrosion issue. He told me that I could wait until the next day for a new heater, or he could install one right now, but I would be without water -- both hot and cold -- for about 6 hours (it takes a while to drain a water heater, and for my place you have to shut down the entire plumbing system in order to get the job done.)