Teaching Kids to Manage Credit: It's as Easy As ABC

Good credit starts at home and spreads abroad -

Well, the old adage actually says "charity" instead of "good credit", but the latter case still rings true. When kids are taught financial literacy and responsibility growing up, they take those lessons with them throughout their lives, eventually teaching their own children.

My mom and dad had no idea that I would need to become financially literate before I left home. My parents had children in their later years, so we are from two totally different generations. Sure, they taught us basic spending and savings skills, but there was not much mention of credit, investments, retirement funding, or anything that "grown up." They simply thought that we had time to learn those things.

They realized that they were wrong when I came home from college with a plummeting credit score and some serious unpaid bills.

There are lots of families, however, who are aware and are taking action early. This recent USA Today article highlights some great strategies that real parents are using to foster fiscal fitness in the lives of their children. I saw some things that I plan on implementing with my little ones when they come of age.

Hopefully, they will learn from my errors and omissions and provide even better training for their children...

Well, the old adage actually says "charity" instead of "good credit", but the latter case still rings true. When kids are taught financial literacy and responsibility growing up, they take those lessons with them throughout their lives, eventually teaching their own children.

My mom and dad had no idea that I would need to become financially literate before I left home. My parents had children in their later years, so we are from two totally different generations. Sure, they taught us basic spending and savings skills, but there was not much mention of credit, investments, retirement funding, or anything that "grown up." They simply thought that we had time to learn those things.

They realized that they were wrong when I came home from college with a plummeting credit score and some serious unpaid bills.

There are lots of families, however, who are aware and are taking action early. This recent USA Today article highlights some great strategies that real parents are using to foster fiscal fitness in the lives of their children. I saw some things that I plan on implementing with my little ones when they come of age.

Hopefully, they will learn from my errors and omissions and provide even better training for their children...

Labels: credit, financial_literacy, I_C_Jackson

|

--> CLICK HERE TO VOTE IN THE DEBT POLL <--

|

posted by I.C. Jackson | 1/30/2008 07:15:00 AM

|

1 comments

links to this post

![]()

![]()

So, the good folks at Discover Financial want us believe that

So, the good folks at Discover Financial want us believe that

My next idea was to take advantage of one of the 0% balance transfer checks that I often receive via snail mail, offers from credit card companies with which I already have an account. In fact, today I got one from Bank of America, and it fit the bill nicely. The balance on my student loan debt is a little over $11,500 (I called for a payoff quote), and this particular Bank of America account has a credit limit that's close to $13,000. All I would have had to do was sign the check, mail it to ED, and the debt would have been transferred to my card. I would have paid no interest on the debt until January 2009. I wouldn't have waited that long to pay it down to zero, however; I would have paid the card off within 4 to 5 months.

My next idea was to take advantage of one of the 0% balance transfer checks that I often receive via snail mail, offers from credit card companies with which I already have an account. In fact, today I got one from Bank of America, and it fit the bill nicely. The balance on my student loan debt is a little over $11,500 (I called for a payoff quote), and this particular Bank of America account has a credit limit that's close to $13,000. All I would have had to do was sign the check, mail it to ED, and the debt would have been transferred to my card. I would have paid no interest on the debt until January 2009. I wouldn't have waited that long to pay it down to zero, however; I would have paid the card off within 4 to 5 months.

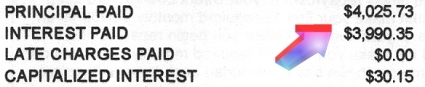

So, last Wednesday, I logged onto the Capital One website to get a payoff quote for my auto loan. On Thursday morning, I visited my local post office and mailed, via overnight express, a check for a tad over $9,000. Today, I was able to login to the Capital One site and confirm that the payment was received. Yahoo. Feels pretty good: I own a great car, and I no longer have car payments (I was paying around $349 per month.)

So, last Wednesday, I logged onto the Capital One website to get a payoff quote for my auto loan. On Thursday morning, I visited my local post office and mailed, via overnight express, a check for a tad over $9,000. Today, I was able to login to the Capital One site and confirm that the payment was received. Yahoo. Feels pretty good: I own a great car, and I no longer have car payments (I was paying around $349 per month.)